Commercial Solar Finance in the UK: A Comprehensive Guide

Published: 2026-07-18 15:50:59

Updated: 2026-07-26 18:19:43

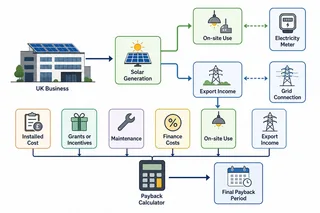

It determines: who funds the installation who owns the solar panels and associated equipment who receives the electricity savings who receives any export.

What commercial solar finance means

Commercial solar finance in the UK is the way a business, landlord, public body, charity, farm, school, care provider, manufacturer, warehouse operator, or other non-domestic organisation pays for a commercial solar PV system.

It determines:

- who funds the installation

- who owns the solar panels and associated equipment

- who receives the electricity savings

- who receives any export income

- who maintains and monitors the system

- who carries performance, roof, insurance, and contract risk

In practice, commercial solar finance is not just a loan or payment decision. It is a combined energy, technical, property, legal, tax, and operational decision. A proposal that looks attractive on monthly payments can be weak if the system exports too much electricity, the roof needs replacement, the grid connection is constrained, or the agreement lasts longer than the occupier’s lease. For UK organisations comparing commercial solar finance options, the key principle is simple: the best structure is the one that fits the site, electricity profile, balance sheet, property position, and long-term plans. A short summary is useful before looking at the detail. Commercial solar finance differs from home solar panel options because projects are usually larger, more site-specific, and more dependent on half-hourly electricity use, landlord consent, grid approval, insurance requirements, tax treatment, procurement rules, and business continuity. what happens if the building is sold, leased, refurbished, or vacated It pays for solar PV on business and non-domestic sites. It can involve ownership by the customer or a third party. It normally relies on reducing imported grid electricity. It must fit the roof, lease, grid connection, and usage profile. It should be assessed over the full system life, not just the headline payback. It should be reviewed alongside tax, accounting, insurance, and property obligations.

The main commercial solar finance options in the UK

The main UK commercial solar finance options are cash purchase, business loan, asset finance, hire purchase, operating lease, power purchase agreement, roof lease, grants, and public-sector funding. The right option depends on capital availability, appetite for ownership, tax position, site control, electricity use, roof suitability, and the length of time the organisation expects to occupy or control the property.

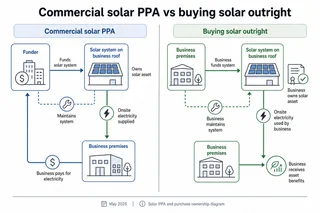

Cash purchase: The organisation pays upfront and owns the system from day one. This can give the strongest long-term return where the site uses a high share of the solar electricity on site. The owner also carries responsibility for maintenance, monitoring, insurance, inverter replacement, performance checks, and any roof-related complications. Business loan: The organisation borrows money to buy the system. Ownership usually remains with the business, but the total cost depends on the loan term, interest rate, security, arrangement fees, repayment profile, and whether repayments match the expected savings. Asset finance and hire purchase: The solar PV system is treated as business equipment and paid for over time. Hire purchase usually means the business owns the system at the end of the agreement, which can suit companies that want predictable payments without using all available capital upfront. Operating lease: The finance provider may own the system during the lease period. The customer may pay a regular rental for use of the equipment. Accounting and tax treatment depends on the precise structure and should be checked with an accountant rather than assumed from the finance label alone. Power purchase agreement: A third party funds, owns, and maintains the solar system, while the site buys the generated electricity at an agreed price per kWh. UK commercial solar PPAs commonly run for long periods and are usually best suited to larger roofs, stable occupation, and strong daytime electricity use. Roof lease: A third party leases roof space and may sell electricity to the occupier or export power to the grid. This is less common for ordinary business roofs unless the roof is large, structurally suitable, and has favourable grid access.

No single structure is automatically best. A cash purchase can maximise savings but uses capital. A PPA can reduce or remove upfront cost but creates a long-term electricity contract. A lease can spread cost but may be harder to align with building sale, roof works, or tenant changes. For many buyers, the most useful comparison is not “which option has the lowest upfront cost?” but “which option gives the best whole-life value with risks we can accept?” Grants and public funding — Grants can reduce upfront cost, but they are usually local, time-limited, sector-specific, competitive, or linked to decarbonisation schemes. Public bodies may have separate funding routes, including public-sector decarbonisation programmes. Blended funding — Some organisations combine internal capital, borrowing, grant funding, and wider energy-efficiency budgets. This can work well when solar is part of a broader net-zero, estates, or energy-cost reduction plan.

How the financial case is assessed

A commercial solar business case is usually built around avoided electricity imports rather than export income. Every unit of solar electricity used on site can reduce the amount bought from the grid, while exported electricity is often worth less than electricity avoided on site.

Indicative UK commercial rooftop solar costs vary by size, roof type, access, electrical works, and site complexity. Smaller commercial systems are often quoted at a higher cost per kWp than larger systems because fixed costs are spread over fewer panels. Larger systems can benefit from scale, but may involve more complex grid, structural, design, metering, or switchgear requirements.

As a broad market guide only, many commercial rooftop solar projects fall within roughly £600 to £1,200 per kWp before project-specific extras and VAT treatment are confirmed. A 50 kWp system may cost materially more or less depending on access, roof condition, electrical infrastructure, and design constraints. A 100 kWp system may achieve a lower cost per kWp than a smaller project, but only if the roof, grid connection, and installation conditions are straightforward. Those figures are only a starting point. Final pricing can change because of:

- roof access and scaffolding

- structural reports or strengthening works

- fragile roof materials and fall protection

- switchgear upgrades

- cable route length

- metering changes

A proper finance model should consider more than simple payback. Useful measures include: For financed systems, the total cost of electricity over the agreement matters more than the monthly payment alone. A low monthly payment can still be poor value if the term is long, indexation is aggressive, maintenance exclusions are wide, or the system is not sized around real daytime demand. Commercial solar output in the UK is commonly around 800 to 1,100 kWh per kWp per year, depending on location and design. Southern England usually produces more per kWp than Scotland or northern England, but roof orientation, pitch, shading, inverter design, soiling, system downtime, and maintenance quality can all affect the result. A credible proposal should show how generation has been modelled and what assumptions have been used. It should not rely only on annual electricity consumption or a generic roof area estimate. fire safety requirements DNO conditions monitoring and data systems design work planning or heritage constraints whether VAT is included, excluded, recoverable, or partly recoverable payback period internal rate of return net present value levelised cost of energy cash-flow impact debt-service cover, where borrowing is used whole-life cost per kWh sensitivity to electricity price changes sensitivity to lower-than-expected generation maintenance and inverter replacement costs

Why self-consumption matters more than export

Self-consumption means the share of solar electricity used directly on site. It is one of the most important variables in commercial solar finance because the value of avoided grid electricity is usually higher than the value of exported electricity.

A site using 70% to 90% of generation on site will usually have a stronger business case than a site exporting most of its generation. This is why factories, warehouses, cold stores, leisure centres, supermarkets, offices, schools, care homes, distribution centres, and many farms can be good candidates when their daytime demand matches industrial solar options.

The Smart Export Guarantee can pay for exported electricity from eligible systems up to 5 MW, but rates vary by supplier and contract. The Feed-in Tariff is closed to new UK applicants, and the Renewables Obligation is closed to new solar PV projects, so older subsidy assumptions should not be used for new business cases. Current export arrangements should be checked directly with suppliers or official guidance before signing a proposal. Export is not worthless, but it is rarely the foundation of a strong commercial rooftop solar case. A system sized only to maximise annual generation may not produce the best financial result if a large share is exported at a lower value. Half-hourly electricity data is therefore important. A full year of half-hourly data shows whether the business consumes power when the panels generate it. It can also reveal: weekend export risk seasonal mismatch summer shutdown periods low-demand holiday periods changes between weekday and weekend use peak daytime loads For commercial solar finance, the quality of the consumption data can be as important as the finance rate. Without accurate usage data, savings forecasts become much less reliable. whether a smaller system might give a better return than filling the whole roof whether battery storage or demand shifting could improve the case

Technical checks funders and installers look at

Commercial solar finance depends on whether the site is technically suitable. Funders and installers will normally want to understand the roof, structure, electrical connection, meter arrangement, grid constraints, access, and ownership position before finalising terms.

A desktop quote based only on annual electricity use is not enough for a reliable finance decision. Real projects need a site survey that checks roof fabric, roof age, access routes, cable routes, switchgear, meter position, plant-room space, fire strategy, and future maintenance requirements.

Important technical checks include the following.

- Roof condition and remaining life.

- Structural capacity and wind loading.

- Shading from plant rooms, parapets, trees, and nearby buildings.

- Skylights, fragile roof areas, and safe maintenance access.

- DNO approval and export capacity.

- Switchgear suitability and cable route length.

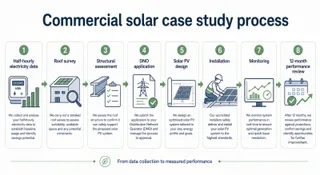

Roof condition is particularly important. Many funders will not finance a system on a roof that is likely to need replacement during the finance term. Removing and reinstalling solar panels for roof repairs can be expensive, disruptive, and contractually complicated. Grid connection is another common constraint. Smaller systems may fit within simpler connection processes if they meet the relevant limits, while larger commercial systems usually require DNO approval before installation. Export limitation can help where the local network cannot accept full export, but it may reduce the value of some generated electricity. Fire safety and insurance requirements should be checked early. Commercial roofs vary widely, and insurers may have specific requirements for DC isolators, cable routes, access spacing, panel layout, monitoring, shutdown procedures, and maintenance records. A proposal should not be treated as final until these issues have been reviewed. For buyer-intent projects, the practical sequence is usually: Skipping these steps can turn an apparently simple solar finance option into a difficult contract later. Insurer requirements and fire safety arrangements. Monitoring, metering, and performance reporting. Roof warranty implications. Asbestos or fragile material risks on older buildings. Planning, conservation, or permitted development constraints where relevant. Future roof maintenance, refurbishment, or redevelopment plans. check electricity demand check roof suitability check structural capacity check grid connection check landlord or freeholder position check finance structure check tax, accounting, and insurance impact compare whole-life value

Landlords, tenants, and building occupation

Commercial solar finance becomes more complicated when the building owner and electricity user are not the same organisation. This creates a split incentive, because the landlord controls the roof while the tenant often pays the electricity bill.

A tenant normally needs landlord consent before installing solar. The lease may restrict roof alterations, plant installation, cable routes, maintenance access, and the right to keep equipment in place. If the tenant has only a short remaining lease, owned solar may be difficult to justify unless there is a clear transfer, extension, removal, compensation, or buyout arrangement.

Landlords can still make solar work, but the structure needs to be clear. The agreement should define: who pays for the system who owns the equipment who receives the electricity benefit who receives export income who maintains the equipment who carries roof repair obligations For a PPA or roof lease, the contract should also explain what happens if the building is sold, the roof needs repair, the occupier changes supplier, the tenant vacates, the site’s electricity demand falls, or redevelopment is planned. Long-term agreements should not be signed without checking that they fit the property strategy. Where the landlord owns the building and the tenant buys the electricity, commercial solar can be structured in several ways. The landlord may fund the installation and recover value through service charges, electricity resale, rent review, or a separate energy agreement. The tenant may fund the installation with landlord consent. A third-party PPA provider may fund the system and sell solar electricity to the occupier. Each route has different legal, tax, and commercial implications. Public bodies, charities, community buildings, schools, healthcare providers, and multi-site organisations may have additional governance requirements. These do not prevent solar finance, but they can affect approval times, procurement routes, documentation, and the evidence funders need. who insures the system who has access rights for maintenance what happens when the tenant leaves

Tax, VAT, grants, and accounting points

Commercial solar is generally subject to VAT. VAT-registered businesses may be able to reclaim input VAT, subject to normal VAT rules, but the treatment depends on the customer, structure, and use of the system.

Tax treatment also depends on ownership and finance structure. Capital allowances may be relevant where the business owns the system, and allowances such as the Annual Investment Allowance or full expensing may be relevant for qualifying expenditure. Leased systems and PPAs can be treated differently from owned systems, so tax advice is important for larger or more complex projects.

Business rates may also need checking. Treatment can depend on how the system is used, whether it mainly supplies the occupier, and whether electricity is exported. Larger systems, landlord-funded systems, and export-heavy systems should be reviewed with a rating adviser rather than relying on a generic assumption. Grants can be useful but should not be treated as guaranteed. UK business solar grants are often local, short-lived, sector-specific, competitive, or tied to wider decarbonisation programmes. Availability can change quickly, and eligibility may depend on location, business size, sector, carbon-saving evidence, procurement timing, and whether work has already started. A project should still make sense without a grant unless the funding has already been confirmed in writing. Organisations should avoid signing a finance contract on the assumption that grant funding will appear later. Accounting treatment can affect how a finance option appears on the balance sheet and profit and loss account. This is especially relevant for leases, PPAs, and asset finance. The commercial decision should be made with input from finance, operations, property, and tax advisers where the project is material. For public-sector and charity buyers, procurement rules, subsidy control considerations, internal approvals, and funding conditions may also influence the finance route. These points should be checked before committing to surveys, legal documents, or long-term electricity contracts.

When commercial solar finance may not be suitable

Commercial solar finance is usually strongest for organisations with stable premises, strong daytime electricity use, a suitable roof or land area, and a long enough planning horizon to benefit from the system. It is not automatically suitable for every business.

It may be a poor fit where the site cannot use enough solar electricity, where the roof is near the end of its life, or where the occupier cannot commit for long enough. It can also be weakened by grid export restrictions, expensive electrical upgrades, difficult access, uncertain trading plans, or uncertainty over future site operations.

Common poor-fit situations include the following.

- Very low daytime electricity use.

- Short leases with no clear landlord agreement.

- Roofs that need replacement soon.

- Weak structural capacity.

- Heavy shading from nearby buildings or roof plant.

- Planned redevelopment or relocation.

Battery storage is another area where caution is needed. Commercial solar battery storage can increase self-consumption, help with peak shaving, support sites with export constraints, or improve use of on-site generation, but it adds cost, degradation, warranty considerations, maintenance requirements, fire safety considerations, and operational complexity. Many commercial solar projects work financially without a battery. EV charging and heat pumps can improve the wider case in some situations, but only if they match the site’s demand pattern. Commercial EV charger installation during daylight can increase solar use. Heat pumps may increase electricity demand more in winter than summer, so their impact should be modelled carefully. Commercial solar finance may also be unsuitable if the organisation is only looking for a short-term saving but the proposed contract creates a long-term obligation. The finance term should match the organisation’s property strategy, expected electricity demand, and appetite for operational responsibility. Grid restrictions that make the system uneconomic. Finance terms that outlast the business need. High installation costs caused by complex access or electrical works. Unclear responsibility for maintenance, insurance, or roof repairs. Large seasonal shutdowns that cause high summer export. Property transactions that could interrupt long-term agreements.

What to check before signing a finance proposal

A good commercial solar finance proposal should be clear about assumptions, responsibilities, exclusions, and long-term obligations. If those points are vague, the headline savings figure is not enough.

Electricity assumptions: The proposal should show the consumption data used, expected self-consumption, export assumptions, degradation, shading, downtime, and any export limitation. Included costs: The proposal should say whether grid applications, surveys, scaffolding, structural reports, design, monitoring, commissioning, VAT, and metering are included or excluded. Ownership and income: The documents should state who owns the system, who receives savings, who receives export payments, and who owns any certificates or environmental benefits. Maintenance and replacement: The agreement should explain who pays for monitoring, servicing, inverter replacement, fault response, panel cleaning, and roof access. Roof works and reinstatement: The contract should define what happens if the roof needs repair, panels must be removed, roof warranties are affected, or the building is sold. Early exit and buyout: The finance terms should state whether early repayment, termination, transfer, or buyout is possible and how the cost is calculated.

For a PPA, the contract should also define the solar electricity price, indexation, contract term, minimum purchase obligations if any, termination rights, buyout method, metering rules, change-of-law provisions, maintenance obligations, and what happens if the occupier’s electricity demand changes. These details have a major effect on the long-term value of the agreement. For asset finance or hire purchase, the buyer should check the total amount payable, ownership transfer, security, early repayment charges, treatment of equipment failure, insurance requirements, and whether maintenance is included or separate. For cash purchase, the buyer should still check warranties, workmanship, monitoring, maintenance, roof access, inverter replacement, DNO approval, and insurance requirements. Paying upfront removes finance costs, but it does not remove technical or operational risk. Insurance and warranties — The proposal should confirm roof warranty implications, insurer requirements, product warranties, workmanship cover, and whether warranties can be assigned. Grid and metering — The project should include DNO approval, export arrangements, generation metering, and any half-hourly or export meter requirements. Performance assumptions — The proposal should show expected annual output, degradation rate, system losses, shading losses, and any availability assumptions. Legal documents — The buyer should review leases, wayleaves, roof access rights, PPA terms, equipment ownership, and security interests before signing. Term length — The agreement should fit the expected site occupation, roof life, business plan, and property strategy. Indexation — Any annual price increases, RPI/CPI links, or fixed uplifts should be clearly modelled over the full term. End-of-term position — The contract should explain whether the system is removed, transferred, extended, bought out, or left in place.

Practical next steps

The best starting point is to gather a recent year of half-hourly electricity data, current tariff information, roof plans if available, lease details if relevant, and any known roof or electrical issues. This allows an installer or finance provider to model the system around real site conditions rather than generic assumptions.

A sensible process is to check the energy profile first, then the roof and structure, then the grid connection, then the finance structure. In real projects, these steps often run in parallel, but none should be ignored.

Before requesting commercial solar finance quotes, UK businesses and organisations should prepare: 12 months of half-hourly electricity consumption data recent electricity bills and tariff details MPAN and meter information roof plans, site plans, or satellite imagery details of roof age, roof type, and known defects lease or ownership information Businesses should compare options on whole-life value, not only upfront cost or monthly payment. A self-funded system may deliver higher long-term savings, while a PPA or lease may suit organisations that want lower capital outlay or third-party maintenance. The right answer depends on the site, the balance sheet, the lease, the electricity profile, the roof, the grid connection, and the organisation’s risk appetite. For a strong commercial solar finance decision, the proposal should answer three questions clearly: If the answer to all three is yes, commercial solar finance can be an effective way for UK organisations to reduce electricity costs, improve energy resilience, and support decarbonisation without relying on outdated subsidy assumptions. planned roof works or redevelopment plans expected future electricity demand changes information on EV charging, heat pumps, refrigeration, machinery, or process loads internal approval requirements and preferred funding approach Will the site use enough solar electricity at the right times? Is the roof, grid connection, and property position suitable for the full term? Does the finance structure improve whole-life value without creating unacceptable long-term obligations?

Plan, Compare & Buy Renewable Energy Solutions

AI does the thinking.

You get the perfect solar match.

Use RoboMo™ to assess your property, compare available technologies and connect with trusted UK installers, suppliers and manufacturers.

Simply enter your postcode, drop a pin on your roof, create your free account and let RoboMo™ analyse your property to find the best solar panels for your home.

You don't have to think

RoboMo™'s AI analyses your roof and does all the hard work.

Accurate & tailored

AI-powered assessment based on your roof, location, and conditions.

Best options, maximum savings

Compare top solar panels for the best performance and value.

Simple, fast & effortless

Provide a few details, sit back and watch your results unfold.

STEP 1

Choose Home, Business or Industrial

Enter your postcode to start your assessment.

STEP 2

Drop a pin on your roof

STEP 3

Create your free account

STEP 4

Sit back and watch RoboMo™ work

RoboMo™ analyses your roof and builds your personalised solar comparison.

Flower Turbines

Design your wind energy system.

Instantly forecast generation.

Choose a location, configure your Flower Turbines and instantly see estimated annual generation using location-specific wind data. No account required.

Real location data

Generation forecasts based on the location you select.

Build your own layout

Configure Flower Turbines to suit your available space.

Instant generation forecasts

See estimated annual generation and energy production instantly.

No commitment required

Explore different configurations before deciding whether to request a quotation.

STEP 1

Enter your postcode

Start designing your wind energy system in seconds.

STEP 2

Choose a location

STEP 3

Build your layout

STEP 4

Instant generation forecasts

Compare different turbine layouts and see annual generation forecasts instantly.

STEP 5

No commitment required

Explore different configurations before deciding whether to request a quotation.

Are you an installer, distributor or renewable energy business?

Kilowatts UK is actively expanding the Flower Turbines partner network across the United Kingdom. Contact us to discuss installation, reseller and project partnership opportunities.

Become A Flower Turbines PartnerRelated articles

FAQ

Need Help? RoboMo's Got Answers

What is commercial solar finance?

Commercial solar finance is the way a UK business or non-domestic organisation pays for a solar PV system. It covers who funds the installation, who owns the equipment, who benefits from electricity savings and export income, who maintains the system, and what happens if the building is sold, leased, refurbished or vacated.

What are the main commercial solar finance options in the UK?

The main options are cash purchase, business loans, asset finance, hire purchase, operating leases, power purchase agreements, roof leases, grants and blended funding. Each option affects ownership, upfront cost, long-term savings, tax treatment, maintenance responsibility and contract risk, so the best choice depends on the site, electricity use, roof condition, property position and balance sheet.

Is it better to buy commercial solar panels outright or use finance?

Buying outright can deliver the strongest long-term return because the organisation keeps the full benefit of electricity savings and any export income. Finance can be useful when a business wants to preserve capital, spread cost over time or use a third-party-funded model such as a PPA. The better option depends on cash availability, finance costs, tax position, site tenure and whole-life value rather than upfront cost alone.

How does a commercial solar PPA work?

Under a commercial solar power purchase agreement, a third party usually funds, owns and maintains the solar PV system, while the site buys the electricity generated at an agreed price per kWh. PPAs can reduce or remove upfront cost, but they are normally long-term contracts and should be checked carefully for pricing, indexation, termination rights, buyout terms, maintenance obligations and what happens if the occupier leaves or electricity demand changes.

What is the difference between asset finance and hire purchase for commercial solar?

Asset finance usually allows a business to spread the cost of a solar PV system over a fixed term, while hire purchase typically gives the business ownership at the end of the agreement after all payments are made. The exact treatment depends on the finance documents, so businesses should check the total amount payable, ownership transfer, security, early repayment charges, insurance requirements and whether maintenance is included.

How much does commercial solar cost in the UK?

Commercial rooftop solar costs vary by system size, roof type, access, electrical works, grid connection requirements and site complexity. As a broad guide, many UK commercial rooftop projects fall around £600 to £1,200 per kWp before project-specific extras and VAT treatment are confirmed, but final pricing can change significantly after structural checks, surveys, DNO review, metering requirements and design work.

What makes a commercial solar project financially viable?

A strong commercial solar business case usually depends on high daytime electricity use, good roof or land availability, a suitable grid connection, manageable installation costs and a finance term that fits the organisation’s plans. The proposal should be assessed using whole-life value, expected self-consumption, export assumptions, maintenance costs, inverter replacement, finance costs, tax treatment and sensitivity to electricity price changes.

Why is self-consumption important for commercial solar finance?

Self-consumption is the share of solar electricity used directly on site. It matters because electricity used on site usually offsets imported grid electricity, which is often worth more than exported electricity. Sites with strong daytime demand, such as factories, warehouses, cold stores, offices, schools, care homes and leisure centres, often have stronger commercial solar returns than sites that export most of their generation.

Can a business earn money from exporting solar electricity?

A business may be able to receive export payments for surplus electricity, for example through eligible Smart Export Guarantee arrangements or a commercial export contract. However, export rates are usually lower than the value of avoiding grid imports, so export income should normally be treated as a secondary benefit rather than the foundation of the financial case.

What checks are needed before financing commercial solar?

Important checks include half-hourly electricity consumption data, roof age and condition, structural capacity, shading, access, cable routes, switchgear suitability, DNO approval, export capacity, metering, insurance requirements, fire safety, roof warranties and any planning or heritage constraints. A reliable finance decision should not be based only on annual electricity usage or a desktop roof estimate.

Can tenants install commercial solar panels?

Tenants can install commercial solar panels only if their lease allows it or the landlord gives consent. The agreement should cover roof alterations, access rights, ownership, maintenance, insurance, export income, removal obligations and what happens when the lease ends. Short leases can make solar harder to justify unless there is a clear extension, transfer, buyout or compensation arrangement.

Can landlords finance solar panels for tenants?

Landlords can finance solar panels for tenanted buildings, but the structure must be clear. The landlord may recover value through electricity resale, service charges, rent arrangements or a separate energy agreement. The documents should define who owns the system, who receives the savings, who maintains it, who insures it and what happens if the tenant leaves or the building is sold.

Are grants available for commercial solar panels in the UK?

Commercial solar grants may be available in some areas or sectors, but they are often local, time-limited, competitive or linked to wider decarbonisation schemes. Eligibility can depend on location, business size, sector, carbon savings, procurement timing and whether the project has already started. A project should normally still make sense without a grant unless funding has been confirmed in writing.

What tax and VAT issues apply to commercial solar finance?

Commercial solar is generally subject to VAT, although VAT-registered businesses may be able to reclaim input VAT depending on normal VAT rules and the project structure. Tax treatment depends on ownership and finance type, with capital allowances potentially relevant for owned systems. Leases, PPAs and asset finance can be treated differently, so businesses should take accounting and tax advice before committing to larger projects.

Does commercial solar affect business rates?

Commercial solar may affect business rates depending on how the system is used, who owns it, whether it mainly supplies the occupier and whether electricity is exported. Larger systems, landlord-funded projects and export-heavy installations should be reviewed with a rating adviser instead of relying on a generic assumption.

How long should a commercial solar finance term be?

The finance term should fit the expected life of the system, the organisation’s site occupation, roof condition, lease term, electricity demand and long-term property plans. A long finance term or PPA can be unsuitable if the business may relocate, the roof may need replacement, the tenant may vacate or redevelopment is likely before the contract ends.

When might commercial solar finance not be suitable?

Commercial solar finance may not be suitable where daytime electricity use is low, the roof needs replacement, the structure is weak, shading is heavy, the lease is short, grid restrictions are severe, installation costs are high or future site use is uncertain. It can also be a poor fit if the proposed contract creates long-term obligations that do not match the organisation’s plans.

Should commercial solar include battery storage?

Battery storage can improve self-consumption, help with peak shaving and support sites with export constraints, but it adds cost, maintenance, degradation, warranty considerations and fire safety requirements. Many commercial solar projects work financially without a battery, so storage should be modelled against the site’s real half-hourly electricity data before being included.

What documents should a business prepare before requesting solar finance quotes?

A business should prepare 12 months of half-hourly electricity data, recent electricity bills, tariff details, MPAN and meter information, roof plans or site plans, roof age and condition details, lease or ownership information, planned roof works, expected demand changes and any internal approval requirements. Better data helps installers and finance providers model a system around real site conditions.

What should be checked before signing a commercial solar finance agreement?

Before signing, check ownership, total cost, finance term, indexation, maintenance responsibilities, inverter replacement, warranties, insurance, roof access, DNO approval, export assumptions, metering, early exit rights, buyout terms, roof repair arrangements and end-of-term options. The agreement should clearly explain what is included, what is excluded and who carries each risk over the full contract term.